Why Are TardFi Bankers Staring at Hyperliquid Charts?

Pre-IPO markets are launching on @HyperliquidX. Can real price discovery happen before Wall Street opens? Can traders enter, exit, hedge, or carry event risk with real counterparties?

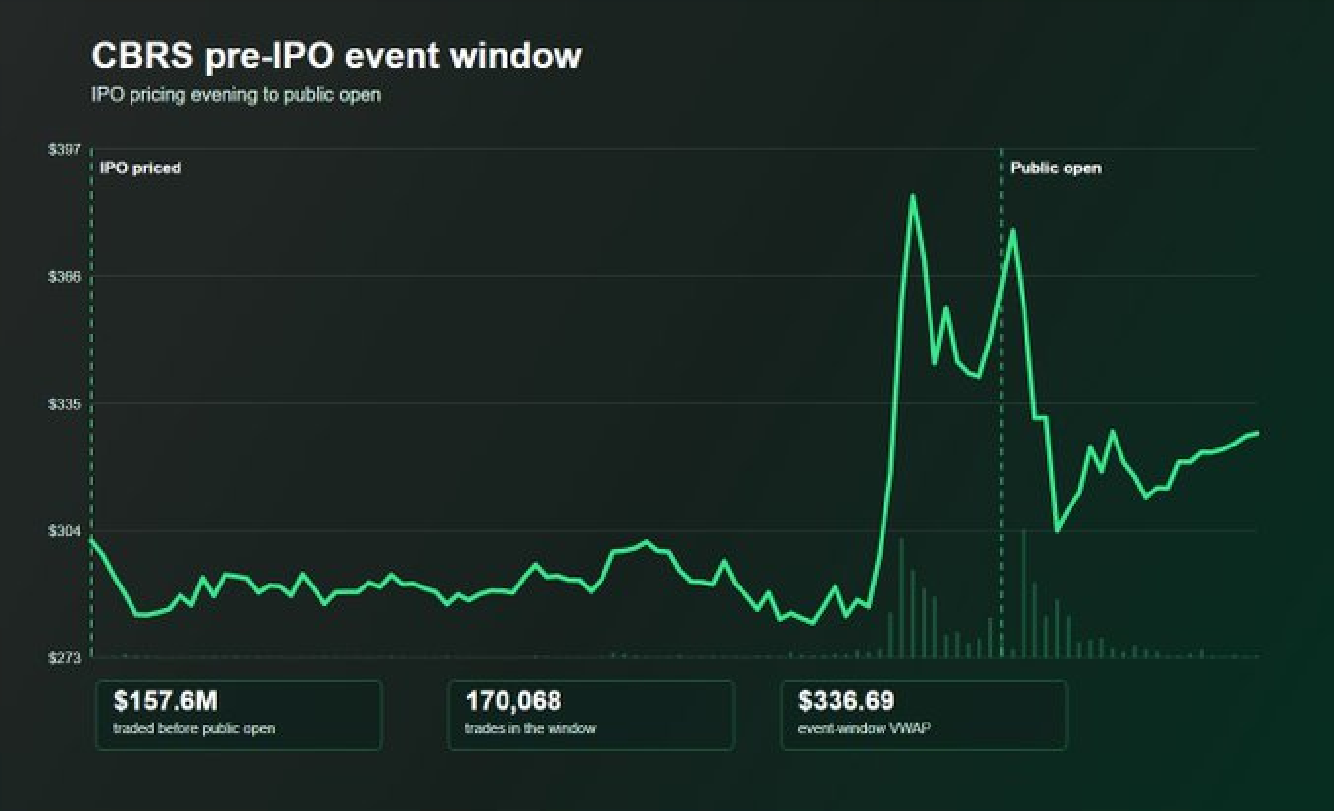

CBRS answered that on-chain on May 13.

Market making pre-IPOs is notoriously difficult. There is no listed secondary venue to lean on. No continuous public tape to arb against. No clean way to offload inventory mid-trade. Wide spreads are how makers get paid for risk they cannot hedge before the stock opens.

From IPO pricing evening to public open, the @tradexyz CBRS market on @HyperliquidX did about $157.60M across 170,068 trades. That number matters because the market absorbed real pre-open risk. The more important question is what liquidity absorbed that risk.

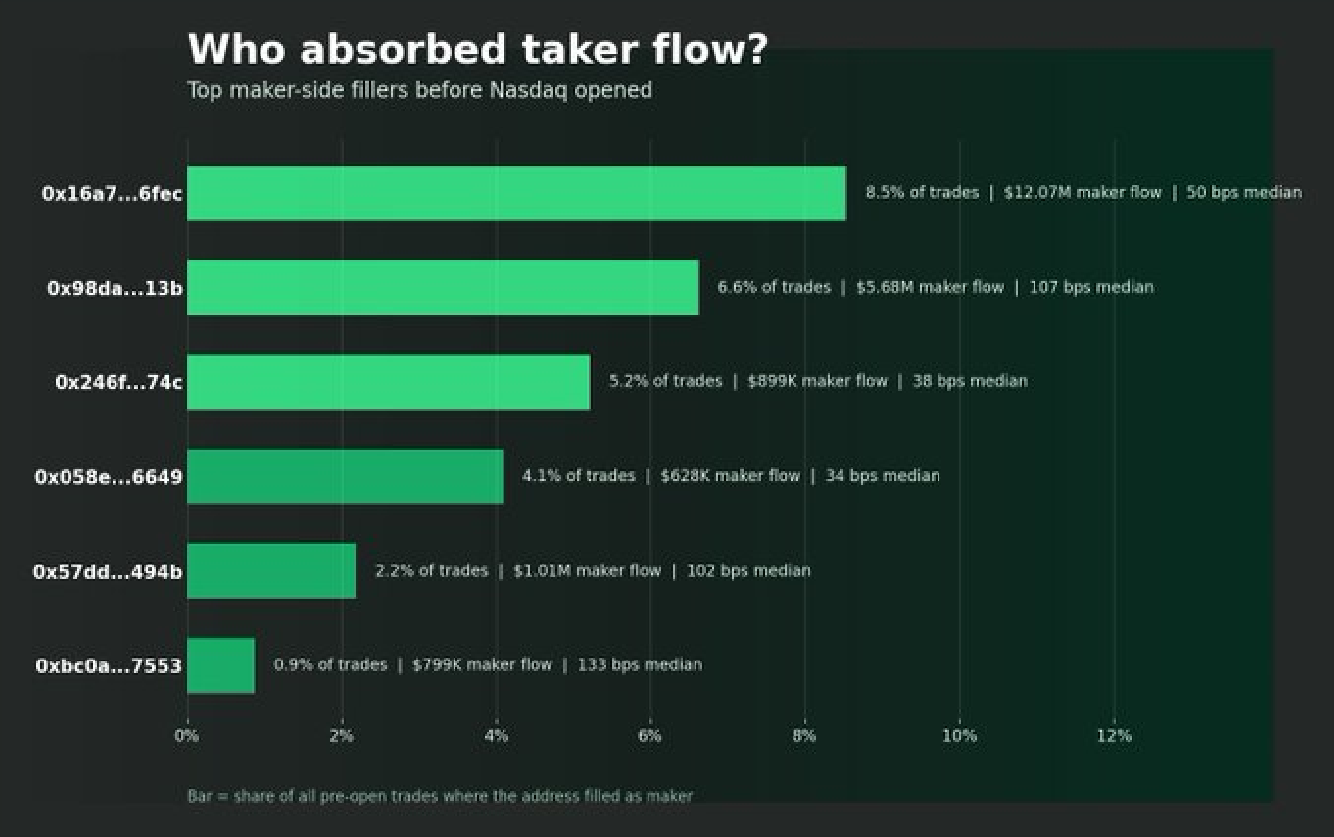

Six active makers each filled at least $250K and filled within 50 bps of mid. Together they filled $15.81M and were maker-side on 18.5% of all pre-open trades.

The largest active maker was 0x16a7...6fec, filling $12.07M and continuously quoting through the pre-open. It was a real counterparty absorbing taker flow, but its median fill was about 49.9 bps from mid, and only about 12% of its maker flow filled within 20 bps.

Another active filler, 0x246f...74c, was maker-side on 5.2% of all pre-open trades across many active periods. 0x98da...13b filled about $5.68M, but its median fill was about 107 bps from mid.

The CBRS pre-IPO market was definitely not cheap to trade. Traders who wanted pre-open exposure were paying at least 50-100+ bps for immediacy, inventory risk, and uncertainty.

What about takers?

Takers were not just one crowd piling into the same trade.

Before the public open, takers opened $52.15M of long exposure and $40.29M of short exposure. They also closed $33.67M of short exposure and $29.97M of long exposure.

Those flows show two different uses of the market at the same time. Some traders were expressing a pre-IPO view. Others were hedging exposure as the event approached.

One clean event-trader example was 0x8652...120d. The bullish whale took $5.60M of liquidity and built long exposure into the public open. At open, the position was down about -$250K. He held the long as it bled PnL before finally capitulating at a -$1.45M loss.

0x9996...91f6 opened $3.17M of short exposure at the public open. That short was briefly marked about -$340K underwater, but PnL turned almost +$800K positive after holding the short steady for 4 days.

0xfe40...4743 had built up $2M of long exposure before the public open. At open, he saw his PnL rocket to $600K and held it for the next 5 days. Over that period, his PnL evaporated, bled to about -$200K, and roundtripped close to par.

0x7d54...2794 opened a $3.28M short at the public open. It was roughly -$200K underwater at the public open, but flipped to about +$800K PnL after holding for 4 days.

So did on-chain pre-IPO price discovery work?

Yes.

CBRS had enough flow for traders to enter and exit meaningful risk with active counterparties taking the other side. It had both long and short demand, and accounts carrying positions throughout.

But it was expensive because it had to be. The market makers took on real inventory risk.

A normal liquid perp should be judged by tightness, depth, and stability near mid. A pre-IPO perp needs a different bar: did it create the best available venue for risk transfer and price discovery before the public market existed?

For CBRS, the answer was yes, but it came with the execution costs that are commensurate with underwriting that kind of pre-IPO risk.

Before @HyperliquidX, the average trader did not have a venue where they could speculate, hedge, or trade pre-IPOs. CBRS showed that a pre-IPO market can exist, attract real market makers, and clear real size before the traditional venue is live.

That is why bankers were staring at the @HyperliquidX CBRS chart at market open: price discovery was happening in public, on-chain, permissionlessly.

Wall Street prices the IPO. @HyperliquidX will be the de-facto exchange to trade that risk.