Bad Oracle, Empty Book: On-chain deep dive into @Ventuals SpaceX blow-up

Ventuals' SpaceX perp dropped 43% in five minutes. Hundreds of retail longs liquidated while the @tradexyz book barely moved. What does the on-chain orderbook data tell us?

TL;DR

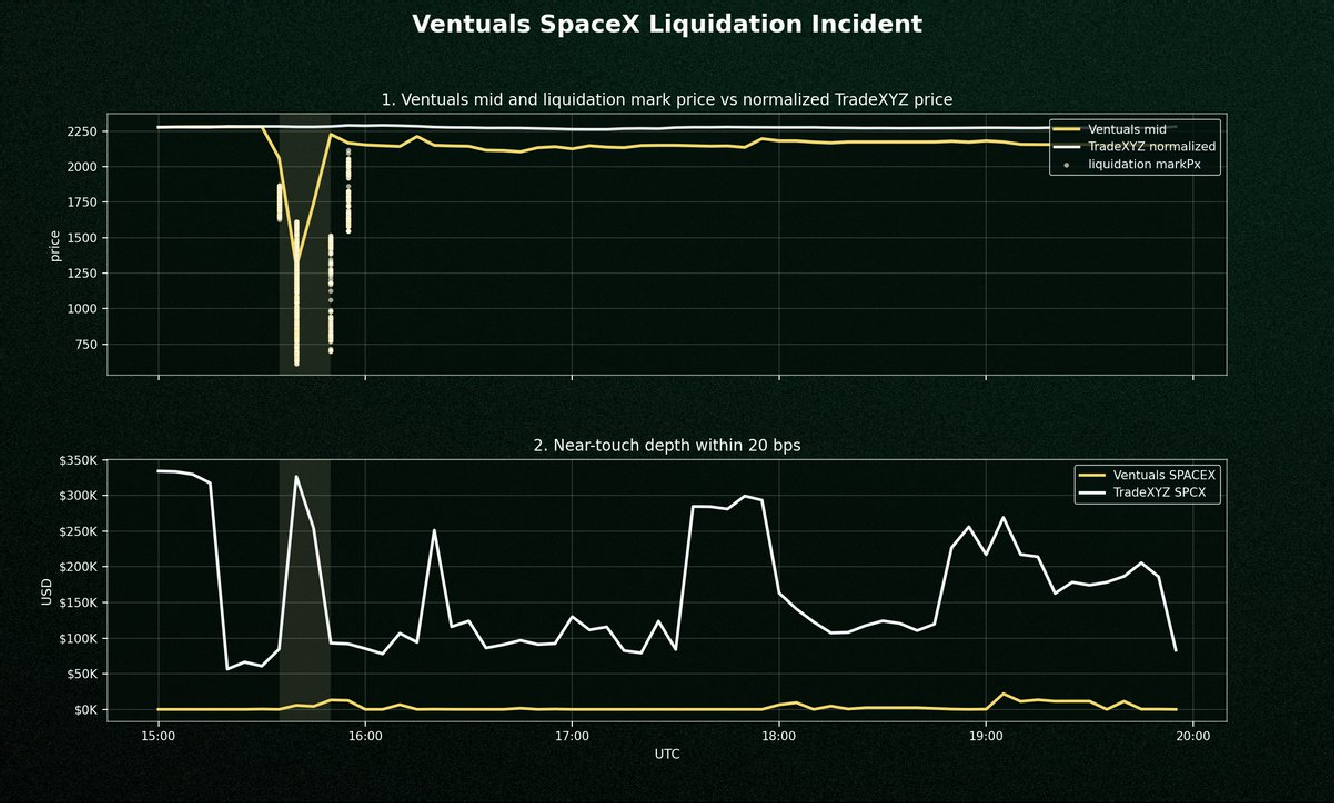

- @ventuals SPACEX perp fell -43.05% in 5 mins.

- @tradexyz (SPCX) drew down just -1.24% with similar orderflow.

- Ventual's book was already broken before the print

- Liquidation marks printed as low as $613.6 against a ~$2,280 reference

- Public reporting tied the trigger to a faulty off-chain oracle feed. On-chain fills show that there was almost no liquidity under the bid

Timeline (UTC)

| Time | Ventuals SPACEX | trade.xyz SPCX |

|---|---|---|

| 15:30 | Mid $2,281.75 | Mid ~$198–200 |

| 15:35 | Bid/ask $1,926 / $2,196, spread 1,310 bps | Remained tightly quoted |

| 15:40 | Mid $1,299.55, $1.61M traded in the 5-min bucket | No matching collapse |

| 15:45 | Mid recovered to $1,742.70 | Held ~$197–199 |

The asymmetry is the whole story. Below is how the two venues compare across the full incident window.

| Metric | Ventuals SPACEX | trade.xyz SPCX |

|---|---|---|

| Max-to-min drawdown | -43.05% | -1.24% |

| Volume | $4.97M | $3.13M |

| Trades | 7,724 | 7,142 |

| Median spread | 40.32 bps | 0.51 bps |

| Median depth within 20 bps | $25 | $123,900 |

Roughly the same notional flowed through both books during the window. @tradexyz held 0.5bps spread with $123K of near-touch depth; Ventuals orderbook was basically empty.

So what happened? A bad print met an empty book

Public reporting stated that one of Ventual's off-chain data providers feed its oracle erroneous data. That explains the trigger. On-chain fills explain why a glitchy print became a liquidation cascade instead of a harmless wick.

1. The book was stressed before the low print.

- Depth within 20 bps: $0

- Depth within 50 bps: $0

Translation: near-touch liquidity was already gone, and forced selling had already started. The market-quality breakdown led the price breakdown.

2. The liquidation mark detached from any sane reference. In the 15:40 bucket, against a $1,299.55 mid:

- Median liquidation markPx: $1,183.1

- Min liquidation markPx: $613.6

A min mark of $613.6, roughly 73% below the reference, showing a oracle/forced-liquidation feedback loop. Longs got marked down to a price the market never actually traded at in size, then closed into a book with nothing under it.

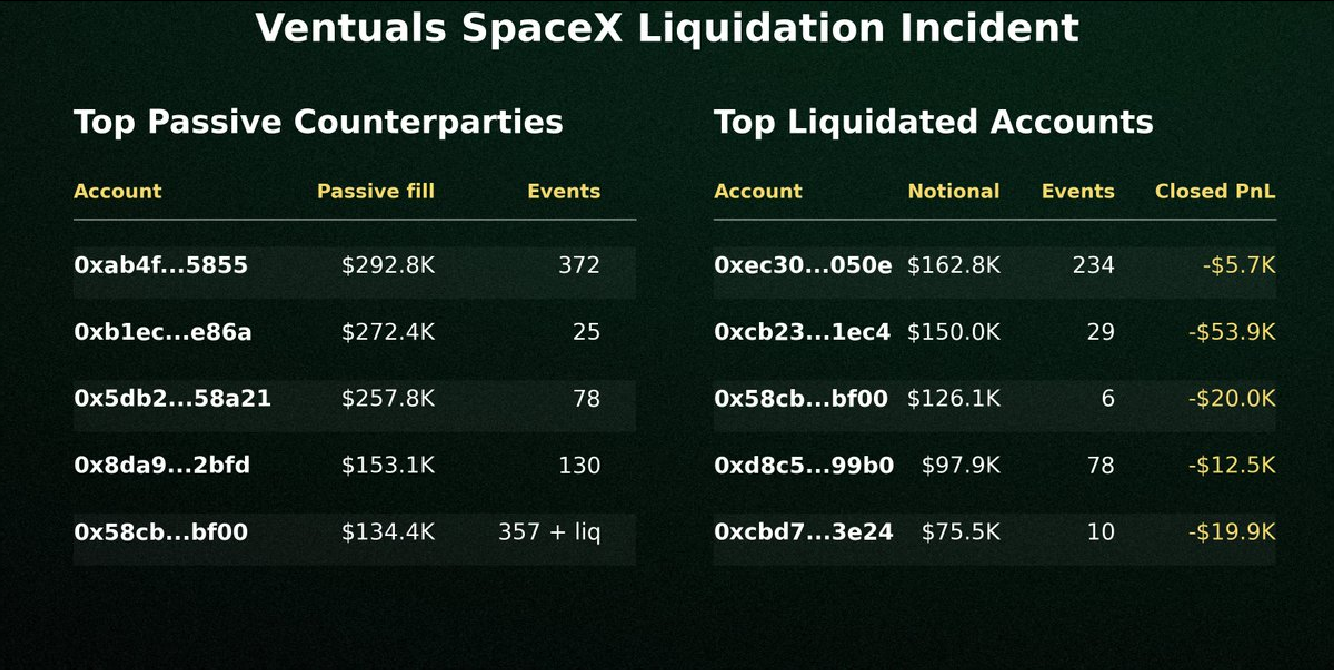

3. A small set of makers absorbed the forced flow. Across the full event the processed fill stream shows 1,611 liquidation trades, $1.74M in liquidated-user notional, 484 unique liquidated users, and 199 passive counterparties. But the absorption was concentrated:

Why trade.xyz didn't blink

Same underlying, same five-hour window, trade.xyz drew down ~1%. The difference is entirely the orderbook liquidity: SPCX ran 0.5bps median spread and ~$124K of depth within 20 bps throughout the incident. If a bad print hits trade.xyz, there would be resting bids to eat it. When it hit Ventuals, there was air.

A thin book doesn't just trade worse on average, it converts an isolated bad tick into a mark-price cascade that liquidates everyone. A few hundred mostly-retail longs, tiny margins, wiped in minutes.

Takeaways for traders

- You're not trading the ticker, you're trading the venue. Read the deployer's price-feed setup and check the order book before you size up.

- Thin books punish leverage non-linearly. An illiquid orderbook means your liquidation doesn't fill near your liq price - it fills wherever the next resting maker is, which could be -50% lower.

- Depth vanishing is the kill signal. When depth within 200bps disappears, the move is coming. Get out.

- Builder-deployed perps are not created equal. Permissionless listing is powerful, but it means oracle quality, maker incentives, and circuit-breaker design vary market to market. DYOR.